Tax compliance and planning are not merely technical obligations buried in accounting departments—they are fundamental expressions of an organization’s ethical posture and strategic foresight. These dual pillars serve as both the shield and compass of modern financial management: compliance ensures that a business meets its legal obligations faithfully, while planning allows it to navigate complexity with prudence and intention. Together, they reflect the heart of responsible Accounting.

On the compliance side, organizations must align their operations with statutory requirements—accurately reporting income, expenses, liabilities, and deductions. This includes timely filing, transparent disclosures, and the maintenance of detailed records that stand up to scrutiny. Compliance is not optional; it is the boundary that separates lawful operation from legal exposure. It is supported by systems such as Auditing and Financial Reporting, which provide validation and public confidence. A clean audit trail, maintained through consistent and honest reporting, becomes a testament to an organization’s integrity.

Planning, however, is where tax becomes not a burden, but a strategic opportunity. Tax planning is not about evasion, nor about loopholes, but about foresight—structuring business decisions in a way that minimizes liabilities within the bounds of the law. Through frameworks grounded in Budgeting and Cost Management, organizations evaluate timing, jurisdiction, capital structure, and resource deployment to optimize their tax outcomes. A well-planned tax strategy can unlock resources for reinvestment, innovation, and long-term sustainability.

In the broader context of Business, Economics and Law, tax consciousness is not confined to the finance department—it permeates all organizational functions. In Business Administration, tax strategy determines whether to expand, consolidate, or restructure. In Finance, it influences capital budgeting, dividend policy, and risk profiles. In Operations Management, it affects supply chain costs and production location choices. In Strategic Management, tax insights feed directly into mergers, acquisitions, and long-term growth trajectories.

Tax also speaks to branding. Consider the influence of tax regimes on Marketing: decisions about pricing, product launch timing, and market entry are shaped in part by fiscal impact. In Business Analytics, tax-related data becomes an input for predictive modeling and KPI analysis. In International Business, differences in tax codes can spell the difference between opportunity and overreach—requiring deep understanding of treaties, withholding taxes, and cross-border compliance.

Managing tax risk is inseparable from strong Corporate Law frameworks. Effective Corporate Governance ensures that tax planning is aligned with company values and stakeholder expectations. Compliance and Regulatory Adherence prevent exposure to legal and reputational damage. Negotiated instruments—like contract negotiation or Mergers and Acquisitions (M&A)—often hinge on tax liabilities, deductions, or deferred credits. Even intellectual property protection carries tax implications in terms of amortization, international licensing, and R&D incentives.

To practice tax planning well, one must look beyond internal affairs and understand the world’s evolving fiscal topography. Knowledge of Economics is essential—not only for understanding macro-trends such as inflation or currency movements but for evaluating the tax environment across sectors. Policy Analysis informs whether legislative shifts are likely to favor capital, labor, or innovation. Meanwhile, Trade regulations dictate how cross-border value chains are taxed and monitored.

Technology plays a pivotal role. Sophisticated data visualization tools and integrated accounting systems enable real-time tracking of tax positions, risk flagging, and reporting accuracy. These platforms strengthen audit trails, highlight discrepancies, and support transparency across departments. In a world where tax authorities increasingly deploy AI and data analytics for enforcement, organizations must match this with digital vigilance and precision.

And finally, tax knowledge is not the exclusive domain of financial elites. It is increasingly taught in education, preparing future leaders in both public and private sectors to engage with tax not as a burden, but as a tool for just and sustainable governance. Tax affects healthcare budgets, educational grants, environmental policy, and more. A society’s tax strategy often reflects its moral vision—who pays, who benefits, and what the system encourages or disincentivizes.

In this light, tax compliance and planning are not mere ledger entries or legal hoops. They are reflections of vision and values—of how an organization, or a nation, chooses to fund its present and shape its future. They are quiet yet powerful forces, shaping decisions, protecting assets, and ensuring that financial ambition walks hand-in-hand with civic responsibility.

A clean, monochrome illustration represents tax compliance. At the center is a tax form with multiple checkmarks, surrounded by calculators, bar charts, upward arrows, a pen, and a business suit silhouette. The imagery conveys accurate calculations, documentation, and verification steps required for proper tax reporting and audit readiness. The overall tone emphasizes organization, transparency, and adherence to regulations.

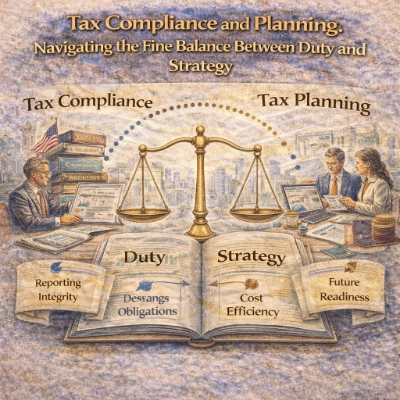

Tax Compliance and Planning: Navigating the Fine Balance Between Duty and Strategy

Tax compliance and tax planning are two sides of the same ethical coin—deeply interwoven practices that define how an organization positions itself in relation to the state, society, and its own future. On the surface, these terms may appear procedural: filing forms, ticking boxes, balancing debits and credits. But beneath this lies a far richer narrative—one of stewardship, transparency, foresight, and adaptation.

To engage in tax compliance is to accept the social contract between enterprise and governance. It is a commitment to act within the boundaries of national and international law, reporting income faithfully and contributing to the shared economic infrastructure. It is a public act of accountability—one that supports public goods, maintains order, and upholds trust in the financial system. Supported by systems like Accounting, Auditing, and Financial Reporting, it ensures clarity in disclosures and integrity in process.

Tax planning, on the other hand, is the art of purposeful foresight. It asks: how might we structure our affairs—legally, ethically, and strategically—to preserve capital, reinvest wisely, and strengthen our financial foundation? It does not defy the law; it works respectfully within it, making full use of allowances, deductions, incentives, and jurisdictional frameworks to support long-term goals. Tax planning is not an evasion of duty, but an optimization of destiny. It is where compliance meets creativity, and where stewardship embraces strategy.

A watercolor-style educational infographic that visualizes tax practice as a balance between obligation and strategy. The composition is split into two halves: Tax Compliance on the left, where a professional reviews forms, records, and supporting documents to represent accurate filing, integrity, and adherence to law; and Tax Planning on the right, where a small team studies charts and projections to represent lawful optimization, reinvestment, and long-term preparation. At the center, golden balance scales sit above an open ledger, with banners emphasizing the twin themes of Duty and Strategy. A softly rendered city skyline in the background reinforces the connection between organizations, governance, and society, while the overall tone communicates stewardship, transparency, and forward-looking decision-making.

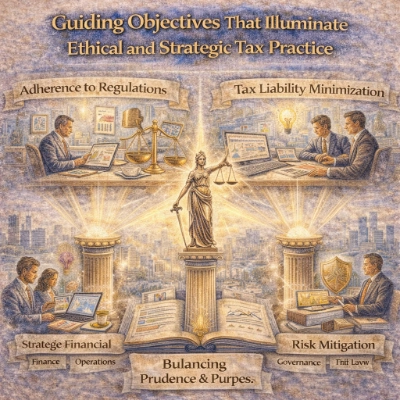

Guiding Objectives That Illuminate Ethical and Strategic Tax Practice

- Adherence to Regulations: Honoring the Rule of Law

The first and most fundamental objective of any tax practice is compliance with the legal frameworks established by tax authorities. This means timely and accurate filings, the correct categorization of income and expenses, and the maintenance of detailed records. Whether you’re a multinational enterprise or a growing startup, failure to comply can lead to fines, audits, reputational damage, or in severe cases, criminal charges.

But beyond fear of penalties, adherence is a form of ethical expression. It declares that the organization is not above the law, but part of a lawful society. Supported by systems of Budgeting and Cost Management and corporate governance, regulatory adherence is the anchor point for everything else—ensuring that tax strategy rests on solid and lawful ground.

- Tax Liability Minimization: Balancing Prudence and Purpose

The second core aim of tax planning is the reduction of tax liabilities within the boundaries of the law. This includes utilizing credits, deductions, deferred income strategies, and choosing appropriate corporate structures. It might mean investing in R&D to take advantage of innovation tax incentives, or timing asset sales to optimize capital gains treatment. Far from unethical, this approach reflects wisdom in resource management.

But here too lies a philosophical tension. Minimizing liability should not erode the spirit of contribution. Ethical planning ensures that reductions in tax burdens do not come at the cost of social responsibility. Organizations must ask not only, “Can we reduce our tax bill?”—but also, “Should we?” In doing so, they elevate tax planning from mere technicality to a matter of principled leadership.

- Strategic Financial Management: Integrating Tax into the Broader Vision

Tax is not an afterthought—it is an integral dimension of strategic financial planning. Whether assessing the feasibility of an expansion, evaluating funding options, or planning a merger, tax implications are ever-present. To ignore them is to risk costly surprises; to integrate them is to build resilience and foresight into financial architecture.

This objective ties directly into other areas of Business Administration, such as Finance, Operations Management, and Strategic Management. A good tax strategy amplifies the impact of corporate initiatives, aligns with long-term goals, and harmonizes fiscal prudence with enterprise ambition. It helps ensure that tax practices support—not contradict—organizational identity.

- Risk Mitigation: Preparing for Uncertainty with Prudence

Tax environments are rarely static. Laws change, audits happen, and global trends can shift overnight. To manage tax risk is to prepare, not panic—to implement controls, document decisions, consult professionals, and anticipate scrutiny. Through proactive monitoring and adaptive strategies, organizations reduce the likelihood of penalties and litigation.

Risk mitigation also connects to corporate governance frameworks, such as Corporate Governance, Compliance and Regulatory Adherence, and sound legal protocols found in Corporate Law. It plays a vital role in situations like contract negotiation, Mergers and Acquisitions (M&A), and intellectual property protection, where unforeseen liabilities can derail even the most carefully planned deals.

When these objectives are embraced—not simply as operational mandates, but as philosophical commitments—tax compliance and planning become instruments of stability, reputation, and wisdom. They allow an organization to walk a path of lawful integrity while advancing its strategic purpose. In an age of regulatory complexity and global interdependence, these practices remain indispensable not only for survival, but for principled and enduring success.

A watercolor-style educational infographic that presents ethical and strategic tax practice as four interconnected objectives. At the center, Lady Justice stands above an open book, symbolizing the rule of law and principled decision-making. Radiating outward are four panels: Adherence to Regulations (a professional reviewing filings and records beside legal scales), Tax Liability Minimization (advisors examining charts and incentives to reduce taxes within legal bounds), Strategic Financial Management (teams aligning tax considerations with finance and operations planning), and Risk Mitigation (a shield and governance cues representing documentation, controls, and audit readiness). Soft cityscape imagery in the background reinforces real-world complexity, while the glowing columns and warm highlights suggest that good tax practice balances duty with strategy through disciplined, ethical stewardship.

The Essential Architecture of Tax Compliance and Planning

Tax compliance and planning are not simply bureaucratic necessities—they are acts of clarity, responsibility, and intelligent foresight. Within these practices lie a deeper promise: to balance civic duty with strategic judgment, and to ensure that individuals and organizations not only survive within fiscal systems, but thrive through them. Below are the essential components that form the pillars of responsible tax conduct, each contributing to the stability, transparency, and ethical resilience of both enterprise and society.

Tax Filing: A Ritual of Disclosure and Discipline

- Definition:

Tax filing is the foundational act of formalizing one’s fiscal obligations. It involves the accurate reporting of income, expenses, deductions, and credits to the appropriate governmental body—typically on an annual or quarterly basis. Filing is more than formality; it is the conscious presentation of truth, supported by evidence, and aligned with the laws of the land.

- Key Features:

- Individual Tax Filing:

From salaried employees to self-employed creatives, individuals must account for income earned through wages, dividends, real estate, or freelance work. Deductions such as charitable donations, home office expenses, or education credits help contextualize one’s tax position within personal life goals.

- Corporate Tax Filing:

Businesses are obligated to report gross revenue, deduct operational expenses, and submit filings that reflect their legal structure—be it sole proprietorship, partnership, or corporation. Here, tax filing becomes a reflection of the company’s internal accounting integrity, supported by Auditing and Financial Reporting.

- Documentation:

Meticulous recordkeeping—receipts, invoices, payroll summaries, bank statements—is the lifeblood of compliant filing. These records serve as both shield and proof in the event of scrutiny or audit.

- Individual Tax Filing:

- Applications:

Meeting filing deadlines ensures lawful standing, avoids penalties, and maintains eligibility for government services or loans.

Many individuals and businesses use tax software or professional services to simplify this process, reducing human error and improving accuracy.

- Examples:

A freelancer submits quarterly estimated tax payments and files a return with deductions for equipment and home office use. See the IRS guide to self-employment taxes.

A corporation completes its annual return, attaching audited financial statements to meet jurisdictional requirements.

Tax Advisory Services: The Intersection of Insight and Intention

- Definition:

Tax advisory services guide individuals and organizations in structuring financial and operational decisions to achieve optimal tax outcomes. More than compliance, this involves anticipation—of regulatory changes, strategic inflection points, and life-cycle events. Advisors operate as ethical navigators, helping their clients walk the fine line between prudence and innovation.

- Key Features:

- Tax Planning:

Advisors identify ways to legally minimize tax liability—through timing of income recognition, use of tax-advantaged accounts, or choice of corporate form. These insights are not merely technical—they shape the strategic narrative of a business or household.

- Incentive Programs:

Governments often reward behaviors that align with public interest. Tax advisory services help organizations leverage R&D credits, renewable energy incentives, or infrastructure subsidies—ensuring the taxpayer’s mission also serves society.

- Tax Risk Management:

Complex strategies must still pass the scrutiny of regulators. Advisors assess compliance risk and documentation rigor to ensure strategies are not only clever, but defensible.

- Tax Planning:

- Applications:

An enterprise invests in clean technologies and leverages energy tax credits to enhance ROI and brand credibility.

An individual contributes to a retirement plan to reduce taxable income while securing long-term savings.

- Examples:

A tech firm claims research tax credits on software prototypes, reducing its tax bill while accelerating innovation.

A family office diversifies investments using capital gains strategies and donation timing to balance taxes and philanthropy.

International Taxation: Aligning Ambition with Sovereignty

- Definition:

International taxation governs the complex, ever-evolving web of rules for individuals and entities operating across borders. It exists at the nexus of national law, global commerce, and sovereign cooperation—and it demands constant vigilance from those who wish to remain agile and compliant in a globalized economy.

- Key Features:

- Transfer Pricing:

When companies transact internally across borders, prices must reflect market realities to avoid profit shifting. Transfer pricing ensures fair allocation of income and taxes across jurisdictions.

- Double Taxation Avoidance:

Bilateral treaties help prevent taxpayers from being taxed by two countries on the same income. Strategic residency and income sourcing decisions are key to leveraging these protections.

- Global Tax Reforms:

International frameworks such as the OECD’s Base Erosion and Profit Shifting (BEPS) initiative aim to close loopholes, enhance transparency, and ensure multinationals pay their fair share where value is created.

- Transfer Pricing:

- Applications:

Firms expand overseas while designing legal and operational structures that avoid excessive tax exposure and regulatory conflict.

Global professionals assess tax residency and reporting obligations in both home and host countries to stay compliant.

- Examples:

A multinational tech company distributes intellectual property licensing revenue through jurisdictions with tax treaties, ensuring both efficiency and legality.

An expatriate entrepreneur declares worldwide income in accordance with U.S. law while claiming foreign tax credits and exclusions.

In sum, these essential components—tax filing, advisory, and international strategy—form a triad of ethical navigation within the financial world. They are not just tools for survival, but instruments of trust, clarity, and vision. To engage deeply in tax compliance and planning is to participate fully in the shared economic project of justice, growth, and sustainable prosperity.

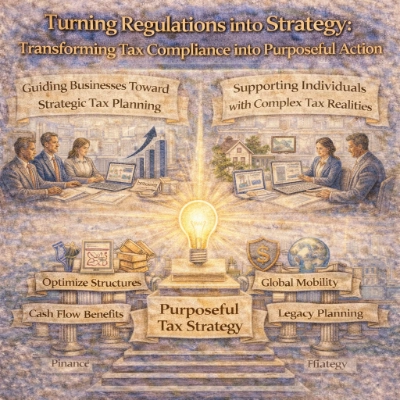

Turning Regulations into Strategy: Transforming Tax Compliance into Purposeful Action

Tax is often perceived as a burden—a set of rules to follow, deadlines to meet, and numbers to calculate. But when approached wisely, tax becomes a tool of transformation. It is no longer merely about compliance; it becomes about strategy, about foresight, and about channeling legal obligations into opportunities for long-term growth. Below, we explore how tax planning is not just a response to regulation, but a conscious act of financial authorship for both businesses and individuals.

Guiding Businesses Toward Strategic Tax Planning

- Overview:

For businesses, tax planning is not a once-a-year formality—it is a continuous exercise in aligning corporate behavior with fiscal intelligence. Organizations use strategic tax advisory to design structures and transactions that not only minimize liabilities, but also support broader operational and ethical goals. Effective planning translates regulation into strategy, risk into readiness, and obligation into resilience.

- Applications:

Designing or restructuring corporate entities to benefit from favorable tax jurisdictions—such as tax treaties, low corporate tax rates, or special economic zones—while maintaining compliance with anti-avoidance legislation.

Planning the timing of capital expenditures or asset acquisitions to take advantage of incentives like accelerated depreciation, which reduce taxable income and improve near-term cash flow.

Using budgeting and cost management tools to project future taxable income and optimize tax-deductible expenses accordingly.

- Examples:

A manufacturing firm invests in automated machinery and leverages the IRS’s accelerated depreciation provisions to significantly reduce its taxable income in the current fiscal year.

A high-growth startup strategically selects a C-corp structure to benefit from lower corporate tax rates and attract venture capital, while planning eventual conversion to an S-corp when appropriate for profit distribution.

Supporting Individuals with Complex Tax Realities

- Overview:

Tax for individuals—particularly those with high incomes, cross-border ties, or significant assets—is rarely straightforward. Strategic planning allows individuals to take control of their tax footprint in a manner that is not only efficient but also aligned with long-term values such as legacy planning, philanthropy, or global mobility. The right plan transforms complexity into clarity and confusion into control.

- Applications:

Rebalancing investment portfolios to favor long-term capital gains and tax-efficient income generation, such as municipal bonds or index funds.

Creating trusts, foundations, or gifting structures to reduce estate tax exposure while maintaining control over intergenerational wealth.

Navigating foreign income, pensions, or real estate holdings with the help of tax treaties and local compliance experts.

- Examples:

An individual creates a charitable remainder trust to provide income during retirement while deferring capital gains and eventually benefiting a nonprofit cause.

A global executive working across three continents leverages double-taxation treaties and foreign earned income exclusions to manage liabilities in both home and host countries.

A watercolor-style educational infographic that frames tax compliance as a pathway to strategic action. The layout is divided into two mirrored halves. On the left, a business team reviews charts and growth projections, representing continuous corporate tax planning—entity structuring, timing of investments, and cash-flow optimization. On the right, advisors work with an individual client, representing complex personal tax realities—portfolio choices, estate and legacy planning, and cross-border obligations. A radiant lightbulb at the center symbolizes insight and foresight, connecting both halves under the theme of “purposeful tax strategy.” Supporting icons—such as a shield with a currency symbol, a globe, and planning documents—reinforce the idea that lawful compliance can be transformed into clarity, resilience, and long-term financial direction.

Scenarios Where Tax Compliance and Planning Come Alive

Tax strategy is not confined to theoretical models or boardroom discussions—it manifests in real decisions, under real constraints, with real consequences. The following practical scenarios show how principles of tax compliance and planning are implemented to turn challenges into advantages and complexity into structure.

Restructuring Corporate Operations for Tax Optimization

- Scenario:

A multinational corporation is expanding operations into Southeast Asia. With the guidance of legal and tax advisors, the company analyzes tax treaties, withholding tax rates, and incentive programs across jurisdictions. It chooses to establish its regional hub in a country with favorable regulations and a robust double taxation agreement (DTA) network.

- Outcome:

By legally shifting income streams and centralizing procurement functions, the corporation reduces its global effective tax rate, improves operational efficiency, and demonstrates full compliance with OECD BEPS guidelines.

Helping Small Enterprises Leverage Deductions

- Scenario:

A small business owner is unsure which business expenses are deductible. With the support of a tax advisor, the owner documents vehicle mileage, home office usage, startup costs, and employee benefit expenses using simple accounting tools.

- Outcome:

The advisor identifies overlooked deductions—such as depreciation on equipment and eligible business meals—which significantly reduce taxable income and increase profitability without crossing any legal boundaries.

Supporting Expatriates Facing Dual Taxation

- Scenario:

An expatriate working in Germany but retaining U.S. citizenship faces taxation by both countries. A specialist tax consultant helps interpret U.S. rules on foreign income exclusions, housing deductions, and foreign tax credits, while ensuring that German filing requirements are satisfied.

- Outcome:

The individual successfully avoids double taxation, remains in full compliance with both tax systems, and gains peace of mind through proactive planning and cross-border documentation.

Together, these examples illustrate that tax is more than a legal requirement—it is a canvas on which financial foresight, ethical judgment, and economic intelligence come together. When applied thoughtfully, tax planning becomes a vital instrument for protecting capital, advancing strategic goals, and contributing to a well-ordered global economy.

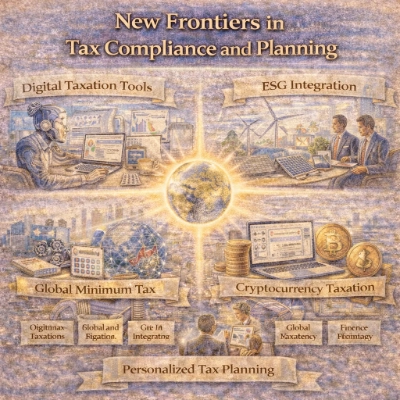

New Frontiers in Tax Compliance and Planning

Tax is no longer a backward-looking process of tabulating expenses and revenues; it is now a dynamic and predictive domain shaped by technology, ethics, globalization, and environmental responsibility. In this new landscape, compliance is not only about avoiding penalties, and planning is not only about reducing liability. Instead, both are being transformed into acts of strategic innovation—where algorithms meet accountability, and tax codes become tools for positive change. Below are the most significant new frontiers redefining the tax space for individuals, businesses, and institutions alike.

Digital Taxation Tools: Automating the Complex, Illuminating the Unseen

Artificial intelligence, machine learning, and robotic process automation are revolutionizing how tax compliance and planning are executed. These tools process vast datasets in real time, flag inconsistencies, and generate insights that human analysts might miss. Automation ensures accuracy, reduces manual labor, and allows tax professionals to focus on judgment and strategy.

Examples include AI-driven audit risk assessment engines that evaluate historical filings for anomalies; real-time tax calculators that integrate with financial management systems; and intelligent filing platforms that auto-populate returns based on categorized expense records.

ESG Integration and Green Tax Incentives: Aligning Profit with Purpose

As businesses become more conscious of their environmental and social impact, tax planning now incorporates ESG (Environmental, Social, and Governance) goals. Governments are increasingly rewarding sustainability with incentives, deductions, and credits—thus making ecological responsibility fiscally prudent as well as ethically sound.

Examples include tax credits for renewable energy investments, deductions for green building renovations, and subsidies for carbon-reduction technologies. ESG-conscious companies now view tax planning not as a standalone task, but as part of a broader mission of sustainable leadership.

Global Minimum Tax Initiatives: A New Era of Fiscal Equity

The OECD’s global minimum corporate tax initiative, part of the ongoing BEPS reforms, seeks to prevent multinational companies from shifting profits to tax havens and eroding national tax bases. This landmark reform marks a philosophical shift: from competition among nations to cooperation for global equity in taxation.

For multinationals, this means rethinking offshore structures, aligning tax reporting with economic substance, and preparing for increased cross-border transparency. For smaller jurisdictions, it invites a reimagining of how to attract investment without engaging in a race to the bottom.

Cryptocurrency Taxation: Bringing Order to the Digital Wild West

Digital assets such as Bitcoin and Ethereum have created new forms of wealth—and new complexities for taxation. Their decentralized nature and volatile pricing make them challenging to track, report, and value. Yet tax authorities worldwide are developing frameworks to ensure transparency and enforce compliance.

Examples include capital gains reporting on crypto trades, tax on mining income, and recordkeeping for decentralized finance (DeFi) transactions. See the IRS guidance on cryptocurrency taxation.

Personalized Tax Planning: Tailored Strategies for a Complex World

Using advanced analytics, tax professionals and platforms can now offer highly customized plans for individuals and businesses. These take into account not only current income but also life goals, risk tolerance, estate plans, and charitable interests. Tax is no longer reactive; it is proactive, evolving with the person or organization it serves.

This is especially vital in a world of hybrid work, global mobility, and fast-changing laws. Personalized planning reflects the growing recognition that one-size-fits-all is obsolete in an age of personal complexity and professional mobility.

A watercolor-style educational infographic that shows how modern tax compliance and planning are evolving. A luminous globe at the center represents global interconnectedness and shared accountability. Around it, themed panels depict: Digital Taxation Tools (automation, AI dashboards, data-driven checks), ESG Integration (renewable energy imagery and sustainability-focused decision-making), Global Minimum Tax (cross-border coordination and fairer global rules), Cryptocurrency Taxation (digital assets and reporting challenges), and Personalized Tax Planning (tailored advisory using analytics to match life goals and complex realities). The overall design emphasizes that contemporary tax work blends technology, ethics, and global frameworks to turn compliance into forward-looking strategy.

Navigating the Complexities of Tax Laws and Policies

As the world grows more interconnected and digital, tax laws are evolving to match. Navigating these laws requires more than compliance—it demands vigilance, flexibility, and a deep understanding of the shifting landscape. Below are key domains where complexity meets consequence, and where thoughtful navigation can mean the difference between risk and resilience.

Evolving Tax Laws: The Only Constant is Change

Tax codes are not static. Legislative changes occur frequently—sometimes driven by political shifts, sometimes by economic necessity, sometimes by global alignment efforts. Organizations must monitor developments to stay compliant and nimble.

Whether it’s an updated depreciation schedule, a new reporting threshold, or revised international treaty obligations, missing an update can trigger penalties or missed opportunities. Tax intelligence is now as critical as tax calculation.

Global Taxation Complexity: When Borders Blur, Risks Multiply

Operating across borders introduces multiple tax authorities, each with unique expectations. Transfer pricing, permanent establishment rules, and currency translation methods all add layers of complexity. Aligning corporate behavior with jurisdictional substance is essential in a post-BEPS world.

Success lies in harmonizing compliance with strategy—balancing regulatory respect with fiscal logic across the globe.

Documentation and Reporting Requirements: The Paper Trail of Legitimacy

In an audit, what matters most is not just what was done, but what was documented. From receipts to tax returns, contracts to intercompany invoices, documentation is the bridge between fact and proof. It tells the story of prudence, process, and preparedness.

Strong documentation practices also allow for proactive defense, rather than reactive explanation. They turn compliance from fear into foresight.

Technological Adaptation: From Manual to Mindful

Tax functions that still rely on spreadsheets and email are falling behind. Modern tax departments must adapt to cloud-based software, integrated compliance platforms, and AI-driven analytics to match the pace of change. This adaptation is not just about efficiency—it’s about survival.

In embracing technology, tax becomes not just faster, but smarter—able to forecast, model, and prevent rather than merely record.

Audit Risk and Preparedness: When Scrutiny is the Standard

Audits are no longer rare or random—they are increasingly data-driven, targeted, and precise. Organizations must be prepared not just for review, but for validation. That means internal controls, audit trails, and documented rationale for tax positions taken.

Mitigating audit risk requires humility in process, clarity in reporting, and agility in response. A well-prepared taxpayer does not fear the audit—they invite it with quiet confidence.

Together, these emerging trends and structural complexities remind us that tax is not simply about rules and rates—it is a language of responsibility and an art of adaptation. Those who master it are not just compliant; they are strategically aligned, ethically grounded, and future-ready.

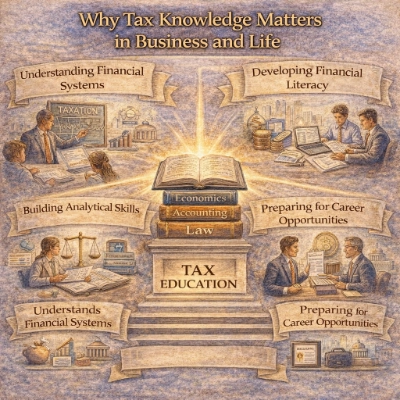

Why Tax Knowledge Matters in Business and Life

Understanding a Key Component of Financial Systems

Developing Real-World Financial Literacy

Building Analytical and Regulatory Awareness

Exploring Ethical and Strategic Dimensions

Preparing for Professional and Academic Opportunities

A warm watercolor infographic that presents tax learning as a foundation for both business understanding and real-life decision-making. At the center, a radiant open book labeled “Tax Education” sits atop stacked volumes titled “Economics,” “Accounting,” and “Law,” symbolizing how tax connects these disciplines. Four illustrated corners expand the message: Understanding Financial Systems (a teacher and students studying taxation with civic and economic symbols), Developing Financial Literacy (people reviewing forms, budgets, and deductions), Building Analytical Skills (careful reading of rules with scales and documents suggesting legal precision), and Preparing for Career Opportunities (a mentorship or interview scene with professional cues). The overall composition emphasizes that tax knowledge builds practical capability, ethical awareness, and readiness for further study and careers.

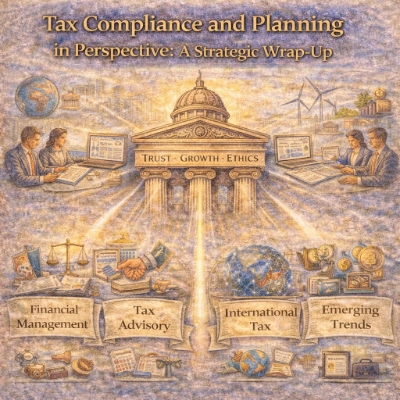

Tax Compliance and Planning in Perspective: A Strategic Wrap-Up

In the grand theater of financial management, few roles are as foundational, misunderstood, or underestimated as Tax Compliance and Planning. To the casual observer, it may seem a dull recital of rules and figures—yet beneath the surface lies a symphony of logic, foresight, strategy, and moral reasoning. Far from being a mere checklist of filings and forms, tax compliance is the expression of civic accountability, while tax planning is the art of harmonizing growth with obligation. Together, they form the pulse that sustains responsible finance, enabling individuals and organizations to thrive within an increasingly complex legal and economic ecosystem.

The Cornerstones: Stability, Legality, and Strategic Intent

At its foundation, tax compliance ensures that one remains within the bounds of national and international laws. It involves the timely and accurate filing of returns, the documentation of income and deductions, and the maintenance of transparent records. This is not simply a matter of avoiding penalties—it is a demonstration of integrity. On the other hand, planning goes beyond compliance, seeking lawful pathways to optimize outcomes. It aligns taxation with broader financial goals, whether that means timing expenditures, leveraging credits, or structuring investments wisely.

Building Blocks of Tax Mastery

Effective tax strategy encompasses multiple domains. It begins with accurate financial reporting, which provides the factual bedrock upon which all tax determinations are made. From there, businesses and individuals engage in advisory services, interpreting the nuances of tax codes and applying them to context-specific challenges. This includes decisions about investment structures, charitable contributions, income deferrals, and use of tax-efficient vehicles such as trusts, pension plans, and tax havens—when appropriate and ethical.

In our globalized economy, international taxation emerges as a critical realm. Cross-border trade, remote work, intellectual property transfers, and multinational supply chains have all introduced new wrinkles into the compliance tapestry. Here, strategies like transfer pricing, treaty application, and the mitigation of double taxation come into play. The goal is not just to reduce burden but to manage exposure, safeguard reputations, and uphold fair contributions across jurisdictions.

Emerging Trends: The Future of Tax Is Already Here

Tax strategy is no longer static or reactive—it is being reshaped by sweeping global currents. Digital transformation, for instance, has introduced artificial intelligence tools that automate filing, detect anomalies, and optimize real-time tax planning scenarios. Compliance is becoming continuous rather than annual, embedded within enterprise systems and financial workflows.

Simultaneously, the rise of ESG (Environmental, Social, Governance) frameworks has woven moral accountability into the fabric of tax. Organizations are now rewarded with green tax incentives for investing in renewable energy, inclusive hiring, and sustainable infrastructure. The notion that taxation is merely an expense is giving way to a vision of tax as leverage—one that supports long-term ecological and social value.

Further, global tax reforms—such as the OECD’s Base Erosion and Profit Shifting (BEPS) initiative and the global minimum tax—are rewriting the rules for multinational corporations. These changes mark a philosophical shift toward fairness and transparency in a world where digital profits often transcend physical borders.

Tax as Strategic Foresight and Ethical Compass

Tax compliance and planning are not just tactical maneuvers. They are manifestations of corporate governance, personal responsibility, and societal trust. For businesses, they can affect investor confidence, customer loyalty, and brand reputation. For individuals, they reflect an understanding of one’s role as a contributor to the common good. At every level, tax choices carry both financial consequences and ethical undertones.

Meticulous tax planning is therefore a commitment to foresight—anticipating legislative changes, modeling scenarios, and adapting to risk. It is also a statement of intent, signaling whether one’s financial structure supports short-term gain or long-term stability. This is especially true for high-net-worth individuals, family-owned businesses, and international firms, where the margin for error is small and the scrutiny great.

The Power of Confidence in a Shifting Terrain

In a tax landscape shaped by uncertainty—economic shocks, regulatory revisions, technological disruption—the greatest asset is not clever loopholes, but confidence. Confidence born from accurate reporting, ethical guidance, strategic insight, and timely adaptation. With the right blend of professional expertise, technological tools, and principled planning, individuals and organizations can navigate even the most intricate tax terrains with assurance.

Final Thought: Beyond Compliance, Toward Contribution

In conclusion, tax compliance and planning are not the end goals—they are means to something greater. When viewed philosophically, tax is a dialogue between the self and the state, between profit and purpose. Those who master its intricacies become not just beneficiaries of financial efficiency but participants in a well-ordered society. Through diligence, creativity, and ethical clarity, tax transforms from burden to instrument—one that serves both personal success and the public good.

A watercolor-style infographic that frames tax compliance and planning as both civic duty and strategic foresight. At the center, a classical courthouse-like structure radiates light and carries the words “Trust • Growth • Ethics,” symbolizing lawful integrity and responsible governance. On the left and right, professionals review dashboards and documents on laptops, representing ongoing compliance, advisory planning, and decision-making. Along the bottom, four parchment banners label key domains—Financial Management, Tax Advisory, International Tax, and Emerging Trends—surrounded by icons such as legal scales, a handshake, a connected globe, digital symbols, and sustainability imagery. The overall scene conveys that modern tax practice integrates standards, ethics, technology, and cross-border awareness to turn regulation into purposeful action.